Originally published on LinkedIn, October 2019

Macroeconomic scenario

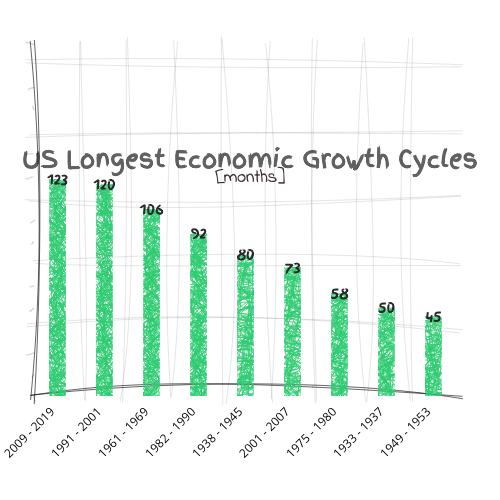

Economic Research institutions worldwide agree that a new recession is about to arrive, but nobody knows when it will arrive. The economy in a capitalistic world follows cyclical patterns, growth periods are followed inevitably by crises periods. The last big recession is now more than ten years old in the US and this has been the longest growth period ever

source: National Bureau of Economic Research

President Trump will be facing the electoral campaign in 2020 and therefore the American Administration will try to all the necessary to avoid a recession before elections, but also the European Central Bank will act to counter the signs of a slowing economy in particular in Germany.

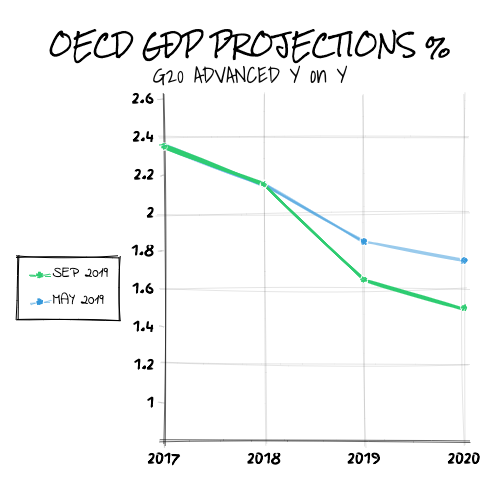

Nevertheless the IMF and the OECD forecast a slowing economy due to several factors and in particular, the persisting risks associated to trade wars between the US and China and the pending BREXIT, in particular, if it will be a hard Brexit.

source; OECD Interim economic outlook 19/9/19

Between May and September growth forecast has been slashed for all the countries and in particular for the most advanced ones

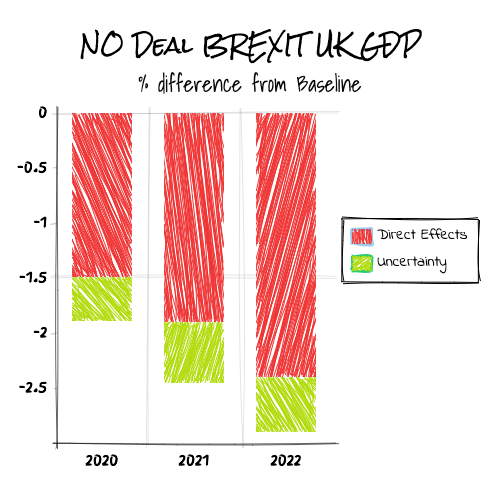

NO-DEAL BREXIT potential impacts in the UK and EU

No-deal Brexit is expected to have a hard impact on the UK economy but also on the EU, and consequently the UK might fall into recession in 2020 with an impact on GDP reaching that might hit a 2% reduction vs previous expectations and British exports to the EU that due to the new tariffs might decline by up to 8%. Tariff impact will be partially recovered by a further 5% depreciation of the pound.

source: OECD Interim Economic Outlook 19/9/19

source: OECD Interim Economic Outlook (19/9/19)

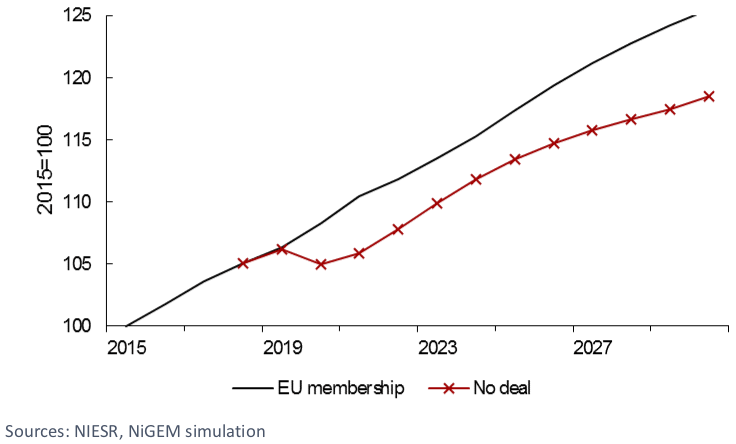

source: NIESR (National Institute of Economic and Social Research 12/9/19)

impact of no-deal Brexit on UK GDP

According to the NIESR institute, the long-run impact of a no-deal Brexit on the UK economy could reach up to 5% compared to "remain" scenario.

Nevertheless, the Economist Global forecasting unit, places the Brexit risk as a low impact and moderate probability, due to the current piece of legislation that has been approved by the British Parliament, the Benn Act, that imposes to the Prime Minister to seek an extension period if the PArliament has not approved a Brexit deal by October the 19th

Commodities: prices expected to decline or have they already reached the floor?

The current downward trend of the major industrial commodities is similar to the trend seen in 2015 and 2016, but the overall price level is higher, and probably hints to an increased capacity of producers to align the offer with the slow down of the demand. In particular, the current trend has been preceded, for several months, by clear signals coming from President Trump policies, that might have triggered a more precise management of production capacities

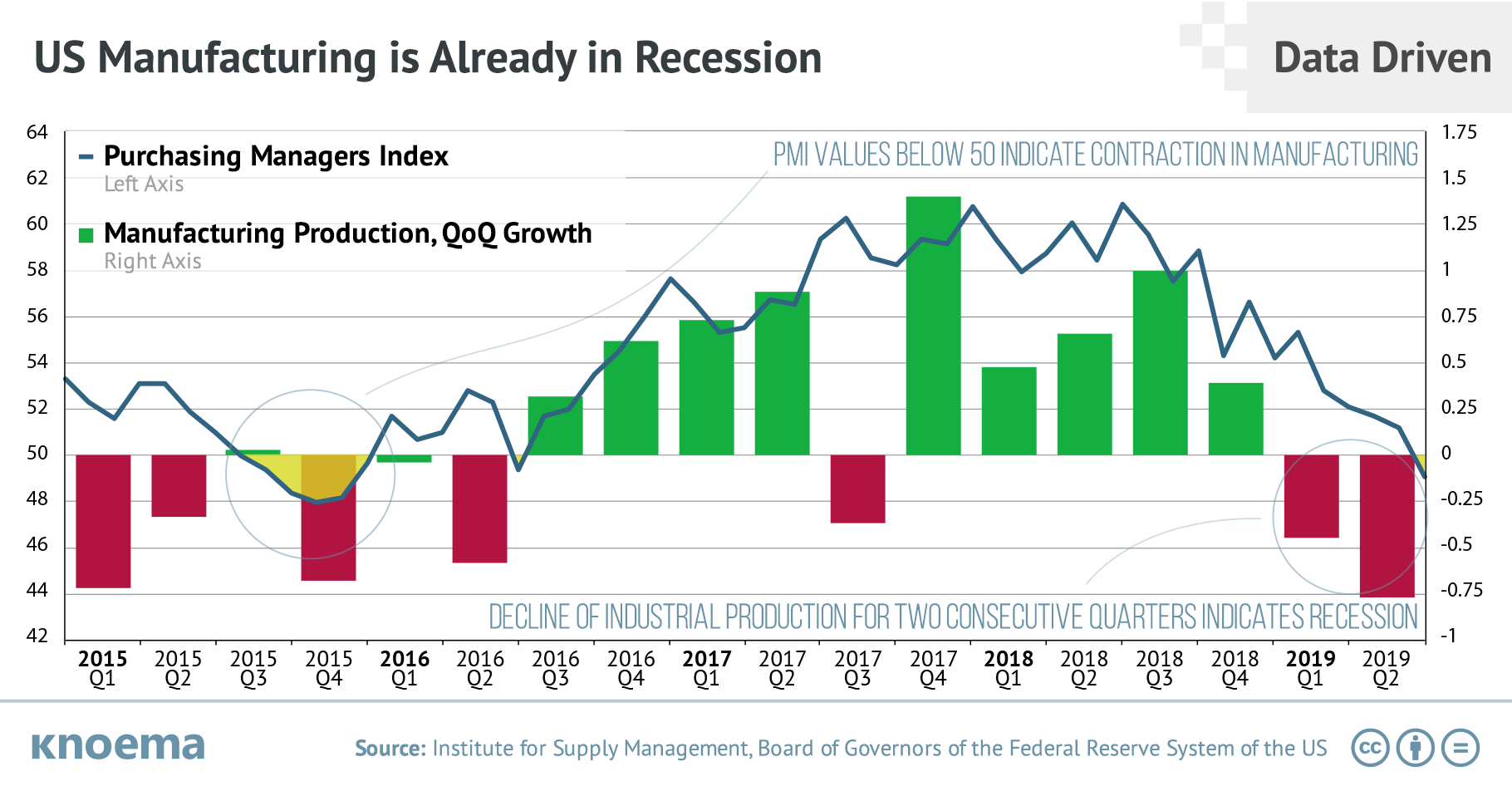

The Purchasing Manager Index (PMI), one of the best indicators to trace macroeconomic dynamics, shows a negative trend in Europe and the USA, while the Chinese index is still somehow stable.

When the index falls below 50 indicates a recession, and the European index is below 50 since Q1 of 2019, while the American index is just passing below that threshold, China is still well above.

Therefore, notwithstanding all the geopolitical factors that have slowed down the demand worldwide (Iran-US crisis, Brexit, China-US trade war, ..), we see that, on the other hand, the Chinese Communist Party is actively engaged in sustaining the internal demand and counter the crises factors and if Trump and Xi Jinping will eventually find an agreement, current stagnation might not turn into a price collapse.

And given that the US and China are by far the world's largest buyers, a similar trend could spread to the rest of the world and in particular Europe.

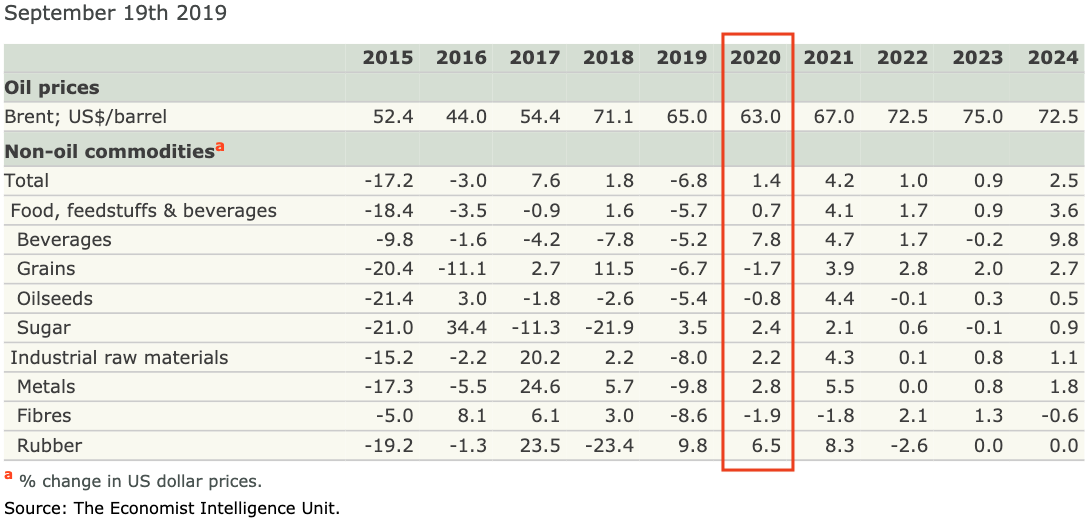

This is the current consensus of major forecasting firms. Here, for instance, we can find the current price forecast from the Economist:

On the same line, the ECB (European Central Bank) forecasts a 3.5% increase of the non-energy commodity prices (in USD) as of September 2019.

Others, like Trending Economics, forecast a general reduction of the prices of the main industrial commodities, but still no brutal reduction.

Energy

According to the US EIA Energy Information Administration, Brent oil price will average $60 per barrel in the fourth quarter of the year, and $63,39 per barrel for the total 2019 and they forecast an oil price for 2020 a $62 per barrel.

The ECB (European Central Bank) forecasts a price of 57 $/barrel and The Economist Global Forecasting Serice is very close to the American forecast with 63 $/barrel (as of September 2019)

There are indications for oil prices for the next year is that it will be driven by four essential factors:

the probability of a global recession that has increased significantly since summer.

an OPEC strategy to continue to cut production.

geopolitical risk in the Middle East after the drone attack on the world's largest oil processing facility in Saudi Arabia.

the effect of the new IMO (International Maritime Organisation) 2020 regulation that has ruled that from 1 January 2020, marine sector emissions in international waters have to be slashed. Given that the marine sector is responsible for half of the global fuel oil demand, the potential impact on prices might be very relevant.

Anyhow, if the EIA (Energy Information Administration) oil price forecast is correct, this price level will not hurt stock prices, the stock market will probably be impacted only if the oil prices hit a minimum of $80 per barrel.

Another point to highlight is that is there is an increase of the geopolitical risk in the Middle East, and this could be a factor that pushes China and the U.S. admiration to reach a trade agreement.

2020 Procurement Budget Assumptions

As of now, the common wisdom seems to be to expect cost factors prices to remain roughly aligned with current prices and even if the world economy is showing many critical signs of stress and "fatigue", it appears to be unlikely that these signs might generate a widespread price collapse. Therefore buyers should not count too much on the possibility to profit from sensibly better conditions delaying the renewal of pricing contract with suppliers. Nevertheless, the possible contraction in the economy might facilitate the definition of contracts to secure stronger relationships with selected suppliers and plan together the cost and conditions improvements that should allow both the customer and the supplier to improve the competitivity level that harsher market conditions might require.